The RBC blog provides inspiring ideas and beneficial strategies to help you prepare for retirement. Additionally, we broadcast timely updates, useful tips & tricks, and vital notifications pertaining to the Retirement Budget Calculator.

The Enhanced Senior Deduction is a new tax benefit introduced by the One Big Beautiful Bill Act (OBBBA) beginning in 2025. It provides an additional $6,000 deduction per person age 65 or older, with income-based phase-outs starting at $75,000 for individuals and $150,000 for married couples filing jointly. This blog post explains how the new deduction works and includes a simple Enhanced Senior Deduction Calculator to help you estimate how much of the deduction you may qualify for under the new rules.

7 Simple exercises to help you plan the best year of your life

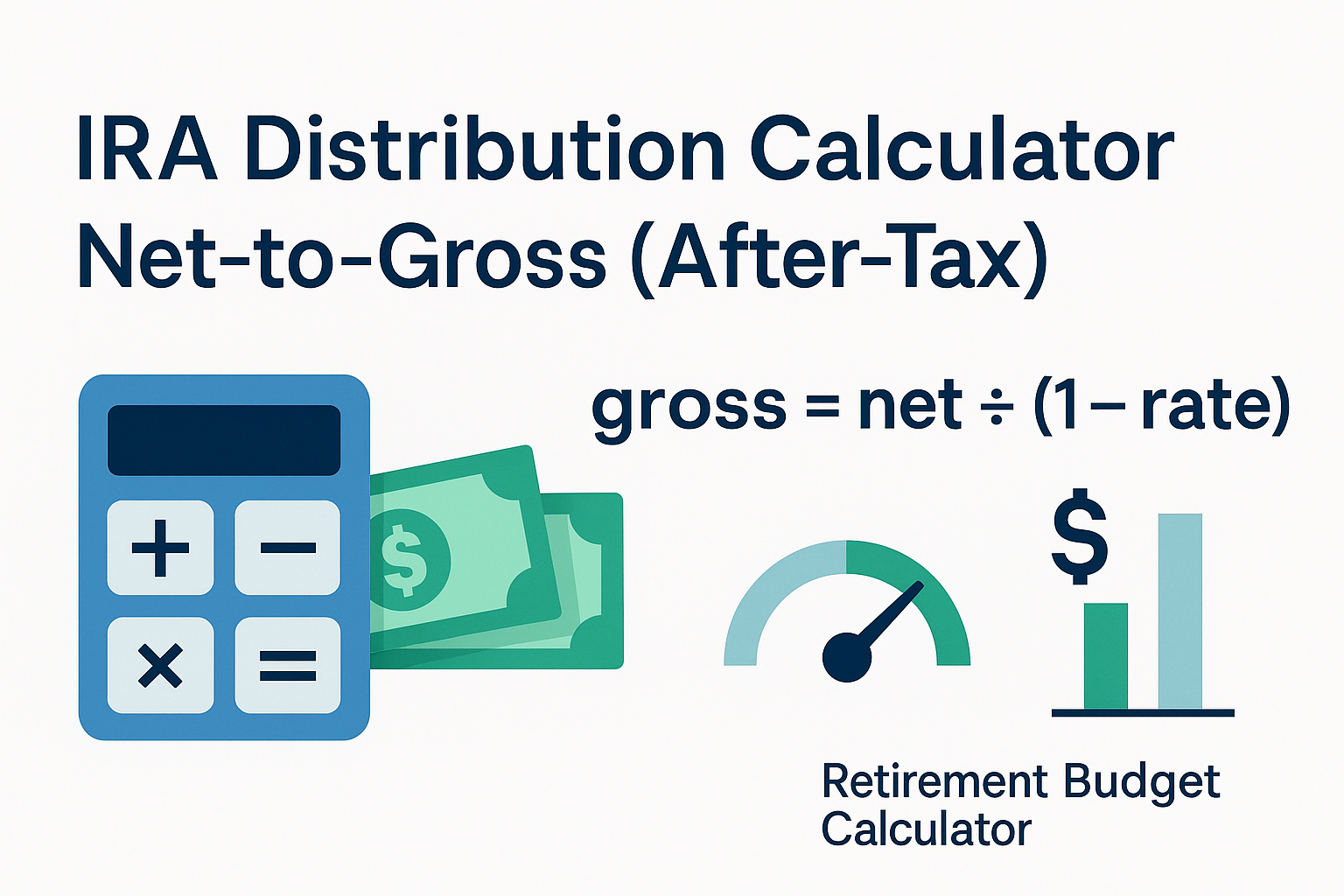

Trying to net a specific dollar amount from an IRA distribution? Don’t guess the gross. Use this simple formula (and our calculator) to back into the right gross amount after withholding. When retirees ask for a certain after-tax amount from their IRA, the most common mistake is adding tax on top of the net. That approach almost always leaves you short. The correct way is to divide the net by what you keep after withholding. This post shows the simple math, a quick example, and the error to avoid—plus an embeddable calculator to do it for you.

The Retirement Budget Calculator is a powerful retirement planning tool with budgeting, tax planning, Social Security optimization, Monte Carlo analysis, withdrawal strategies, and more. Plan your retirement with confidence.

The Federal Employee Health Benefits (FEHB) program is one of the most valuable retirement benefits for federal employees, but understanding how it works after you leave service is key to maximizing its value. To keep FEHB in retirement, you must retire on an immediate annuity and have been enrolled for the five years before retirement. The government continues to pay most of the premium, but retirees lose the pre-tax advantage, making premiums feel more expensive. While pensions receive annual cost-of-living adjustments, they often lag behind the faster rise in FEHB premiums, creating long-term budgeting challenges. Coordinating FEHB with Medicare—especially Part B—can provide broad protection, with FEHB acting as a “super supplement” for services Medicare doesn’t cover, but the decision depends on personal health, income, and risk tolerance.

If you're turning 73 or 75 soon, understanding Required Minimum Distributions (RMDs) is essential for managing your retirement income and taxes. This post explains when RMDs begin, how they’re calculated using the IRS Uniform Lifetime Table, and includes tables showing both distribution factors and their equivalent withdrawal percentages. Plan ahead to avoid penalties and optimize your retirement cash flow.

If one spouse files for Social Security early and the other delays until age 70, it’s still possible to receive a higher spousal benefit — but only if you understand how the rules work. This post explains how early filing reductions, spousal top-up benefits, and survivor benefits interact, using a real-life example to show how strategic timing can significantly impact retirement income for couples.

The blog post outlines 12 surprising lessons that retirees often encounter as they transition into retirement.

In this blog post, we explore the importance of managing expectations and embracing market volatility by analyzing 20 years of data from the Russell 3000 Index. Through a historical lens, we highlight how understanding past market trends can help investors maintain a balanced perspective, avoid emotional decision-making, and stay committed to long-term financial goals. The post emphasizes the value of realistic expectations, diversification, and having a solid financial plan to navigate the inevitable ups and downs of the stock market with confidence.

No retirement budget is complete without factoring in Social Security Income. But deciding when to take Social Security can be a challenge. These are the four questions to answer before filing for Social Security.

The bucketing strategy divides a retirement portfolio into different risk segments called buckets. Retirees can use their cash bucket to cover their day-to-day budget needs. The remainder can be invested in riskier assets to promote growth to cover a retiree's future needs.

Having a good budget will help you have more confidence as you prepare for retirement. Here is a list of the 7 primary categories when planning for retirement.

Getting a late start to retirement savings can make a comfortable retirement seem impossible. But people in their 40's, 50's and 60's can still take steps to make the retirement budget work.

Preparing to retire can cause worry and uncertainty. An easy to use retirement calculator with great visuals can help provide a better understanding of retirement readiness.

Downsizing homes is one way to cut expenses and grow your nest egg in retirement. But downsizing can lead to some unexpected budget changes.

The financial side of retirement planning can be a challenge. A retirement budget calculator with personalized charts can help you see whether you're on track to retire.

A retirement calculator can help people who are ages 55-64 keep a close eye on the numbers that matter the most as you are preparing for an early retirement.

After the launch of the retirement budget calculator dashboard last week we had a really tremendous response and I just wanted to take a minute a highlight a few of your comments.

Retirement Benchmarks allow you to review your financial information and compare it with standard benchmarks so that you can accurately assess how prepared for retirement you are.

In this video we explain why retirement is all about cash-flow and how you can use the retirement budget calculator to create a retirement plan that will give you more confidence as you prepare for retirement.